Awareness around this practice has risen substantially in recent years, but how can investors determine if it’s a good fit for their portfolio? To answer this question, MSCI has identified three common motivations for using ESG in one’s portfolio, which have been outlined in the graphic above.

The Three Motivators

According to this research, the three primary motivations for ESG investing are defined as ESG integration, incorporating personal values, and making a positive impact. These goals are not mutually exclusive, though, and an investor may relate to more than just one.

#1: ESG Integration

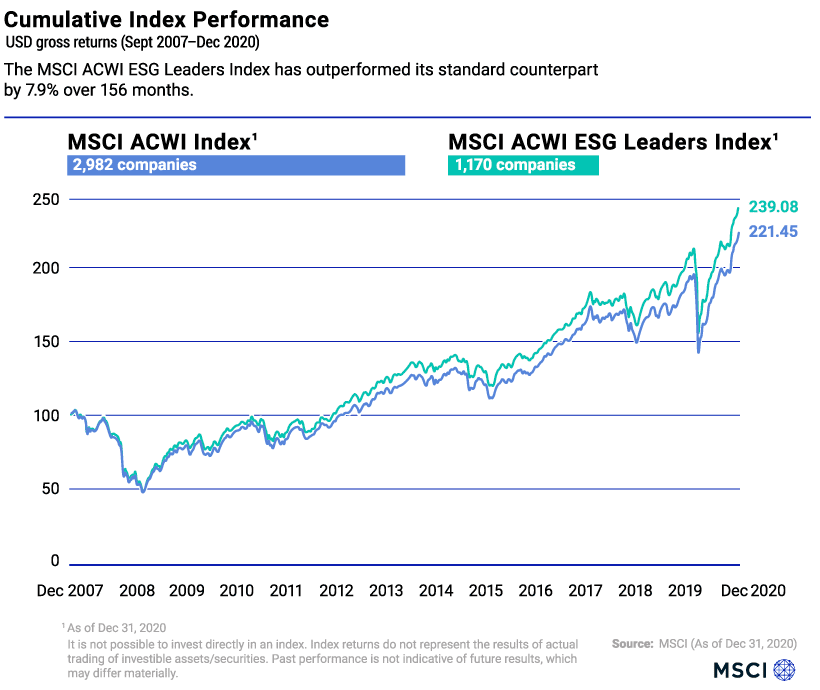

This motivation refers to investors who believe that using ESG can improve their portfolio’s long-term results. One way this can be achieved is by investing in companies that have the strongest environmental, social, and governance practices within their industry. These companies are referred to as “ESG leaders”, while companies at the opposite end of the scale are known as “ESG laggards”. From a social perspective, an ESG leader could be a firm that promotes diversity and inclusion, while an ESG laggard could be a company with a history of labor strikes. To show how ESG integration may lead to better long-term results, we’ve compared the performance of the MSCI ACWI ESG Leaders Index with its standard counterpart, the MSCI ACWI Index, which represents the full opportunity set of large- and mid-cap stocks across developed and emerging markets.

The MSCI ACWI ESG Leaders Index targets companies that have the highest ESG rated performance in each sector of its standard counterpart. The result is an index with a smaller number of underlying companies (1,170 versus 2,982), and a relative outperformance of 7.9% over 156 months.

#2: Incorporating Personal Values

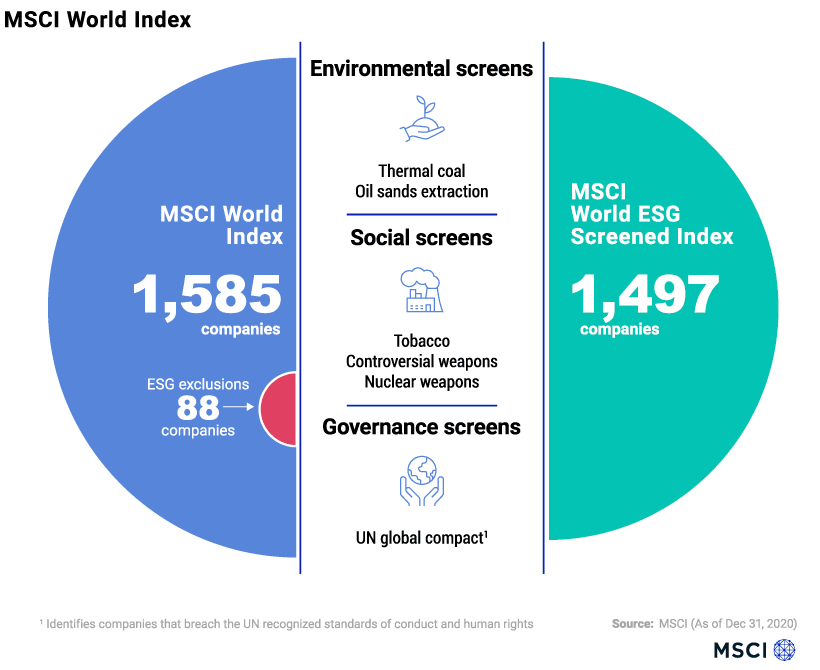

ESG investing is also a powerful tool for investors who wish to align their financial decisions with their personal values. This can be achieved through the use of negative screens, which identify and exclude companies that have exposure to specific ESG issues. To see how this works, we’ve illustrated the differences between the MSCI World ESG Screened Index and its standard counterpart, the MSCI World Index.

The MSCI World ESG Screened Index excludes companies that are associated with controversial weapons, tobacco, fossil fuels, and those that are not in compliance with the UN Global Compact. The UN Global Compact is a corporate sustainability initiative that focuses on issues such as human rights and corruption.

#3: Making a Positive Impact

The third motivation for using ESG is the desire to make a positive impact through one’s investments. Also known as impact investing, this practice enables investors to merge financial gains with environmental or social progress. Investors have a variety of tools to help them in this regard, such as the MSCI Women’s Leadership Index, which tracks companies that exhibit a commitment towards gender diversity. Green bonds, bonds that are issued to raise money for environmental projects, are another option for investors looking to drive positive change.

ESG Investing For All

With various angles to approach it from, ESG investing is likely to appeal to a majority of investors. In fact, a 2019 survey found that 84% of U.S. investors want the ability to tailor their investments to their values. Likewise, 86% of them believe that companies with strong ESG practices may be more profitable. Results like these underscore the high demand that U.S. investors have for ESG investing—between 2018 and 2020, ESG-related assets grew 42% to reach $17 trillion, and now represent 33% of total U.S. assets under management. on Last year, stock and bond returns tumbled after the Federal Reserve hiked interest rates at the fastest speed in 40 years. It was the first time in decades that both asset classes posted negative annual investment returns in tandem. Over four decades, this has happened 2.4% of the time across any 12-month rolling period. To look at how various stock and bond asset allocations have performed over history—and their broader correlations—the above graphic charts their best, worst, and average returns, using data from Vanguard.

How Has Asset Allocation Impacted Returns?

Based on data between 1926 and 2019, the table below looks at the spectrum of market returns of different asset allocations:

We can see that a portfolio made entirely of stocks returned 10.3% on average, the highest across all asset allocations. Of course, this came with wider return variance, hitting an annual low of -43% and a high of 54%.

A traditional 60/40 portfolio—which has lost its luster in recent years as low interest rates have led to lower bond returns—saw an average historical return of 8.8%. As interest rates have climbed in recent years, this may widen its appeal once again as bond returns may rise.

Meanwhile, a 100% bond portfolio averaged 5.3% in annual returns over the period. Bonds typically serve as a hedge against portfolio losses thanks to their typically negative historical correlation to stocks.

A Closer Look at Historical Correlations

To understand how 2022 was an outlier in terms of asset correlations we can look at the graphic below:

The last time stocks and bonds moved together in a negative direction was in 1969. At the time, inflation was accelerating and the Fed was hiking interest rates to cool rising costs. In fact, historically, when inflation surges, stocks and bonds have often moved in similar directions. Underscoring this divergence is real interest rate volatility. When real interest rates are a driving force in the market, as we have seen in the last year, it hurts both stock and bond returns. This is because higher interest rates can reduce the future cash flows of these investments. Adding another layer is the level of risk appetite among investors. When the economic outlook is uncertain and interest rate volatility is high, investors are more likely to take risk off their portfolios and demand higher returns for taking on higher risk. This can push down equity and bond prices. On the other hand, if the economic outlook is positive, investors may be willing to take on more risk, in turn potentially boosting equity prices.

Current Investment Returns in Context

Today, financial markets are seeing sharp swings as the ripple effects of higher interest rates are sinking in. For investors, historical data provides insight on long-term asset allocation trends. Over the last century, cycles of high interest rates have come and gone. Both equity and bond investment returns have been resilient for investors who stay the course.